The Automotive Industry at a Crossroads

Recently I have been collaborating with Stephen Zoepf, Executive Director of the Center for Automotive Research at Stanford on the challenges facing the incumbent automotive industry because of the emergence of new business models and technologies. The piece below is the first of what we hope to be a series.

The automotive industry has survived many swings of feast and famine using a business model that is largely unchanged in a century. The industry has made a remarkable recovery in the decade since the Great Recession, with record sales and profits over the past five years. Yet despite this success, there is broad recognition something fundamental has changed and that focusing exclusively on the current business model is unwise.

After decades of stability, the automotive value chain is being challenged by a storm of social problems to which transportation is a contributing factor, including rising urban congestion, road fatalities and climate change. Simultaneously, the industry is being pulled in new directions by promising technological developments: electrification, automation, artificial intelligence and high-speed wireless connectivity. Leaders of automotive companies are now contemplating how to migrate from their current business model.

Why is change even attractive in the first place? Few if any mobility companies are making a profit. The industry has already invested $80B in autonomy and a similar amount may be necessary before today’s limited trials become revenue-generating deployments. In on-demand mobility services Uber alone has burned $14B of capital and currently accounts for under 1% of vehicle miles traveled. Full electrification of the fleet (currently <2% of new US vehicles sales) may require another $300B.

Despite massive investments that will be necessary on top of the large sums that have been invested, there is optimism about the future profitability of Mobility as a Service (MaaS). In addition to providing potential solutions the social problems mentioned above, on-demand mobility companies are able to provide consumers solutions to problems that automotive companies have not solved: the stress of driving, paucity of parking, and high fixed costs of car ownership. Moreover, these companies establish a more intimate relationship with their customers than automotive companies ever had: they know a customer’s regular destinations and travel schedule. They have access to a customer’s payment data, and know what a customer is willing to pay for a trip. They even know the phone numbers of a customer’s important contacts. This type of customer familiarity has long been recognized as a way to extract more from an industry value chain.

The MaaS value chain remains a primordial soup full of unknown potential, but three key structures are emerging as components of the forthcoming MaaS ecosystem:

- Vehicles: regardless of how they are owned, powered and operated we will still need physical objects to carry people and goods.

- An Autonomous OS: the combination of sensors, servers and software to operate a vehicle without a human driver.

- The mobility marketplace: a platform in which users can view transportation options and order a ride.

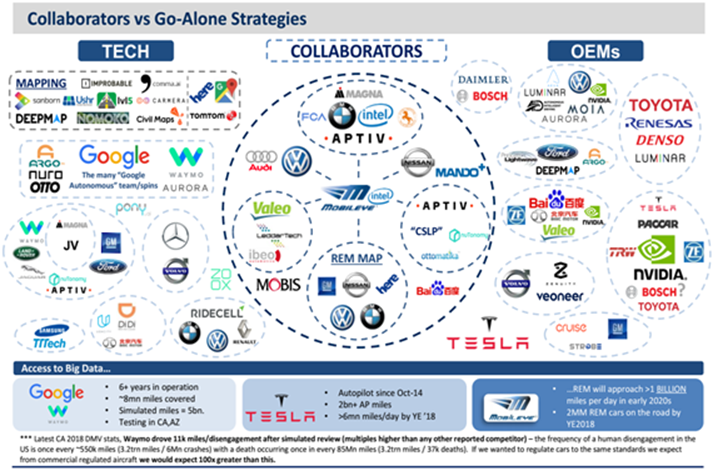

Less clear is what combination of companies, markets, and regulatory bodies will deliver these core structures, and how economic benefit will agglomerate. Still unclear about the role they want to play in new mobility and how much money they will invest, the incumbent automotive industry is entering into a series of uneasy alliances with technology companies and emerging MaaS ecosystem participants. Several of these alliances are shown in Figure 1. Consider the situation currently being tested in Las Vegas: Lyft offers ride-hailing services in autonomous vehicles supplied by BMW and equipped with an AV Stack provided by Aptiv.

Should MaaS be a concern to the automotive industry or should the industry participate in this model by being more than a vehicle supplier to it? MaaS transportation may not lead to reduced vehicle sales but it could negatively impact the OEMs’ volume-based economics nonetheless. In this respect, while MaaS may not be a direct competitor to the automotive product, it is certainly a threat to the profitability of the automotive business model.

- MaaS companies further separate automotive manufacturers from their existing customers

- Vehicle attributes that OEMs pride themselves in may cease to be important to MaaS users, eliminating product differentiation and margin.

- MaaS fleet managers could pit OEMs against each other, leveraging volume to reduce manufacturer margins.

- Tier-one suppliers may be able to compete with traditional manufacturers by providing vehicles directly to MaaS operators.

Automotive manufacturers have always had to invest heavily in new technologies that found their way to vehicles. Several OEMs are now investing aggressively in new mobility and have embarked on broad experimentation. These experiments include startup investments, partnerships, and acquisitions. Some experiments quickly proved unsuccessful. For example, Ford acquired Chariot, a microtransit service, and after operating it for a short period in a few cities it closed it down. But it has built upon its acquisitions of Livio and Autonomic that are considered successful. Similarly, BMW recently decided to merge its ReachNow mobility services unit with Daimler’s Car2Go. However, other experiments continue and even expand. For example, GM and Ford are expanding the tests of their autonomous vehicle ride-hailing service in more cities, Ford is starting to experiment with last-mile delivery, and Toyota has expanded its ride-hailing investments in Uber and Grab,

Automotive manufacturers can and do invest but face four fundamental constraints on how rapidly they can innovate around on-demand mobility:

- Capital: Vehicle manufacturing is enormously capital intensive. While cars generate billions of dollars in revenue, they also require billions to develop and manufacture. Large investments in new business models require sacrifices in conventional R&D: cutting model lines, shuttering plants, and possibly jeopardizing competitiveness in the core business.

- Skill Set: Automotive manufacturers are lacking much of the key expertise to operate a MaaS service or build an autonomous vehicle stack. Obtaining the right mix of talent to preserve the core business while building a new one will be a key challenge.

- Culture: It will require patience for OEMs to determine which of these experiments are proving successful and thus warrant continued investment and support in order to evolve them into new businesses. It will also take fortitude in order to accept that certain experiments need to be eliminated. The culture of large corporations in general and incumbent automakers in particular, that favor stability over agility, is not going to help and may prove one of their biggest liabilities in their effort to decide which path to follow.

- Regulation: The changing regulatory environment, such as the EU’s CO2 emissions regulations, as well as the emerging trade wars create additional issues that have to be addressed as OEMs ponder their future role in consumer transportation

As we are about to enter this century’s second decade, the incumbent automotive industry has arrived at a crossroad. The path it decides to take has the potential to impact it for the next 50 years. Its decisions may have to be based less on its experiences of the past 100 years but on lessons it can extract from other industries such as retail, telco, and media that found themselves in similar crossroads. These decisions may enable the industry to thrive for the next 50–100 years or may lead to its rapid shrinking. The CEOs, management teams, and boards of directors of these companies have their work cut out for them.

Leave a Reply